El Cerrito’s financial story is starting to feel familiar.

On paper, the numbers appear solid. The City reports $22.6M in total reserves, but just $9.3M—17% of expenditures—is held as General Fund reserves per policy. That sounds stable.

But the real question isn’t whether the policy is met today. It’s what’s happening around it.

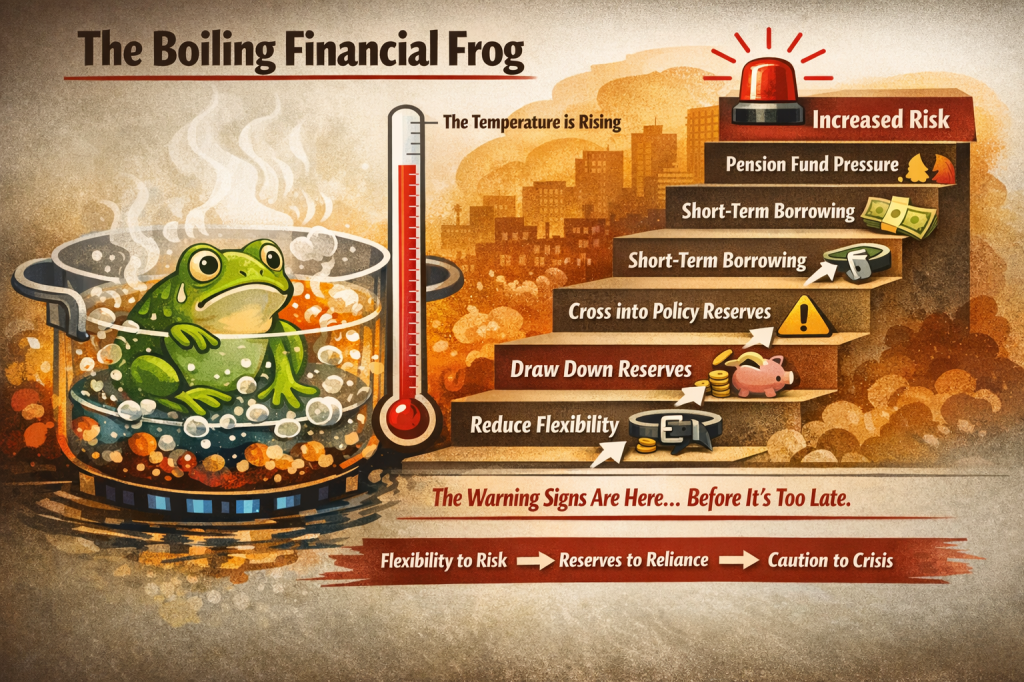

Right now, the City is acting like the frog in cold water—comfortable, because nothing feels urgent. But the temperature is rising.

The City is planning to spend more than it brings in this year. Revenues are projected at approximately $53.8 million, while expenditures exceed $54.6 million, with additional costs—like pool renovations—pushing the gap even wider.

That results in a projected drawdown this year of about $2.8 million.

But that number understates the real trend.

When viewed over multiple years, the City is likely drawing down reserves at a rate closer to $2.5M to $3.0M or more annually.

That’s the pattern that matters.

Because that drawdown doesn’t come from the policy reserve itself—at least not yet.

It comes from what sits above it.

After accounting for restricted funds like the $7.5 million Emergency and Disaster Recovery Fund and roughly $3 million in the Section 115 pension trust, the City’s remaining unassigned balance sits at about $11.9 million.

Of that, $9.3 million is already committed to meeting the City’s 17% reserve policy.

What’s left—about $2.6 million—is the City’s remaining flexibility.

And that flexibility is already being used.

At the current pace, that discretionary buffer could be depleted within roughly a year.

But it doesn’t stop there.

If the underlying imbalance remains, the City won’t simply stop spending—it will continue to draw down reserves.

And that means crossing into the $9.3 million policy reserve.

At current trends, it is entirely plausible that by next year the City will no longer meet its own 17% reserve policy.

That’s the inflection point.

Because once the policy reserve is no longer maintained, the conversation changes—from managing flexibility to managing risk.

The water is getting warmer.

Nothing collapses overnight. There’s no dramatic moment where alarms go off. Instead, the City slowly loses flexibility—year by year, decision by decision.

And by the time the heat is undeniable, the options are already limited.

Because once the General Fund reserve begins to erode, the next step becomes increasingly predictable.

As financial pressure builds—particularly from rising pension costs—the City may begin looking beyond the General Fund for relief.

That puts the Section 115 pension trust in focus.

The Section 115 trust is intended to stabilize long-term pension obligations and protect against volatility. It is a financial safeguard, not an operating backstop.

But under sustained pressure, it can begin to serve a different role.

Not by design—but by necessity.

As pension costs continue to grow, the City may rely on the Section 115 fund to offset those increases and relieve pressure on the General Fund.

And while that may provide short-term budget relief, it comes with a long-term cost.

It reduces the City’s ability to manage future pension volatility and weakens one of its key financial safeguards.

In other words, it shifts risk forward.

If this feels familiar, it should.

In the years leading up to 2018, El Cerrito experienced a similar pattern. Spending pressures outpaced revenue growth. Reserves were gradually drawn down to sustain operations. The City remained fiscally compliant on paper—but with less and less flexibility.

And as that flexibility narrowed, reliance on short-term borrowing increased.

Tax and Revenue Anticipation Notes—TRANs—became a more prominent tool.

TRANs are often used responsibly to smooth timing differences between revenues and expenses. But when paired with declining reserves, they can signal something else: a system under strain.

Less cash on hand means less margin for error.

Less margin for error means greater dependence on borrowing.

And borrowing, even short-term, comes with costs and constraints.

This is how structural issues begin to surface—not all at once, but gradually.

Draw down reserves to cover gaps

Reduce financial flexibility

Cross into policy reserves

Increase reliance on short-term borrowing

Shift pressure to pension stabilization funds

Face growing pressure to stabilize the system

We are not at that point today.

But the trajectory is clear.

Because the City is not rebuilding reserves—it is using them.

And if current trends continue, the shift from flexibility to risk may happen sooner than many expect.

The lesson from 2018 isn’t that the system failed.

It’s that the warning signs were there—quiet, gradual, easy to ignore.

Just like now.

The question isn’t whether the water is boiling.

It’s whether we recognize the temperature is rising—before the City moves from managing its finances to reacting to them.