El Cerrito’s Proposed Budget Reveals a City Under Growing Structural Pressure

El Cerrito’s proposed biennial budget deserves credit for one important thing: it is more candid than some prior financial discussions about the pressures the City is facing.

The problem is that honesty alone does not eliminate the risks.

Beneath the balanced-budget presentation is a much tighter financial picture than many residents may realize, one shaped by escalating pension obligations, thin operating margins, aging infrastructure, rising labor costs, and shrinking flexibility.

This is not a fiscally comfortable budget.

It is a fiscally constrained budget attempting to stabilize itself while carrying significant long-term obligations.

Pension Costs Remain a Major Long-Term Risk

The City Manager openly acknowledges pension escalation through the early 2030s.

That section deserves scrutiny because it leans heavily on a future “PEPRA relief” narrative.

The assumptions are:

• legacy employees retire

• newer employees have lower pension formulas

• long-term costs eventually stabilize

That may partially happen.

But what the budget underemphasizes is that several major cost drivers continue rising simultaneously:

• Public safety staffing remains expensive

• salary inflation compounds pension obligations

• CalPERS investment assumptions can change

• unfunded liability payments can spike during downturns

• healthcare and workers’ compensation costs continue rising

The numbers themselves tell the story.

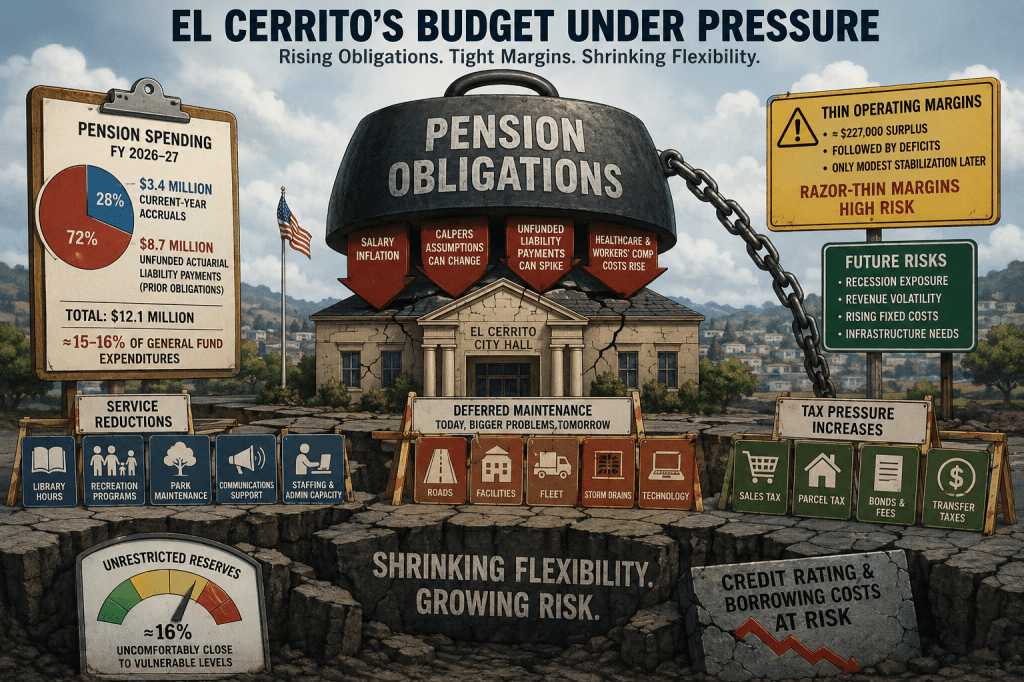

El Cerrito budgeted approximately $12.1 million in total CalPERS pension contributions for FY 2026–27. Of that:

• approximately $3.4 million is for current-year pension accruals

• Approximately $8.7 million is for unfunded actuarial liability payments tied to prior obligations

That means roughly:

• 28% of pension spending funds are current employee retirement accruals

• 72% goes toward pension debt from prior obligations

Even more importantly, pension costs now consume roughly 15–16% of General Fund expenditures.

That is a very large share of the operating budget for a single fixed-cost category.

And most of it is not for current services. It is debt service on prior obligations.

The budget also projects only extremely thin future operating margins:

• approximately $227,000 in surplus

• followed by deficits

• followed by only modest stabilization later

Those are razor-thin margins for a city simultaneously facing:

• pension escalation

• infrastructure aging

• labor negotiations

• insurance inflation

• emergency risk

• recession exposure

This budget is not fiscally comfortable.

It is fiscally tight.

Pension Costs Are Not Optional

One of the hardest realities in municipal finance is that pension obligations cannot simply be deferred indefinitely without consequences.

Cities can reduce:

• recreation programming

• communications budgets

• beautification

• training

• events

• discretionary staffing

• maintenance schedules

But pension obligations are legally and contractually required.

That distinction matters enormously because fixed obligations steadily consume a larger share of operating resources over time.

The result is often a slow but persistent squeeze on services and flexibility.

Service Reductions Become Structural

As pension costs consume a larger share of the operating budget, cities often:

• reduce library hours

• defer road maintenance

• cut recreation programs

• reduce park maintenance

• leave vacancies unfilled

• reduce administrative capacity

• shrink planning or permit support

• delay technology upgrades

The budget already hints at this dynamic through:

• reduced events

• reduced janitorial services

• reduced communications support

• lower discretionary spending

Those are often early-stage containment measures.

Over time, the pressure can move into core service levels.

Deferred Maintenance Accelerates

This is one of the biggest long-term risks.

When pension obligations rise faster than revenues, cities often postpone:

• facility repairs

• fleet replacement

• road rehabilitation

• storm drain upgrades

• HVAC replacement

• technology modernization

That creates a hidden liability.

The budget itself acknowledges that reserve accumulation did not adequately occur for certain replacement needs, including fire equipment planning.

Deferred maintenance can temporarily “balance” budgets, but eventually, small problems become major capital emergencies.

Tax Pressure Increases

When structural pension costs rise persistently, cities often turn toward:

• sales taxes

• parcel taxes

• bonds

• assessment districts

• fee increases

• transfer taxes

El Cerrito already relies heavily on:

• Measure G sales tax revenue

• transfer taxes

• parcel taxes

• special revenue mechanisms

If pension pressure continues growing while service expectations remain high, future tax pressure becomes increasingly likely.

Budget Flexibility Shrinks

One of the hardest things about pension obligations is that they are largely inflexible.

During recessions:

• revenues may fall sharply

• but pension payments usually do not fall proportionally

In fact, after market downturns, pension contributions often rise.

That creates a dangerous financial squeeze:

• falling revenues

• rising fixed costs

• growing infrastructure needs

This is why reserve levels matter so much.

The City is projected to approach approximately 16% unrestricted reserves, uncomfortably close to levels many finance professionals would view as vulnerable for a city facing substantial fixed obligations and economic uncertainty.

A city with thin operating margins can become vulnerable very quickly during an economic downturn.

Credit Ratings and Borrowing Costs Can Be Affected

Rating agencies pay close attention to:

• pension liabilities

• reserve levels

• structural balance

• revenue volatility

• fixed-cost burdens

If pension costs become too dominant relative to revenues:

• borrowing costs can rise

• bond ratings may weaken

• Financing infrastructure becomes more expensive

For a city with significant infrastructure obligations, that matters a great deal.

Labor Negotiations Become More Difficult

As pension and benefit costs rise, future compensation negotiations become more constrained.

Cities often face tensions between:

• maintaining competitive compensation

• avoiding layoffs

• preserving services

• managing pension obligations

This can affect:

• recruitment

• retention

• morale

• staffing stability

especially in public safety positions.

The City Can Enter a “Managed Decline” Cycle

This is the long-term risk many residents never fully see because it happens gradually.

The pattern often looks like this:

• costs rise steadily

• Discretionary services shrink slowly

• maintenance is deferred

• taxes increase periodically

• staffing becomes tighter

• infrastructure ages

• residents feel services slipping

• trust erodes

while budgets technically remain “balanced.”

That is why structural balance matters so much.

A technically balanced budget can still mask long-term erosion if fixed obligations steadily consume larger portions of revenue.

Future Councils Lose Flexibility

One underappreciated consequence is that today’s obligations reduce tomorrow’s choices.

Future councils inherit:

• required UAL payments

• pension schedules

• deferred maintenance

• debt service

• labor obligations

before they even begin discussing new priorities.

That can make local government feel increasingly reactive instead of strategic.

In Extreme Cases, Fiscal Emergencies Occur

El Cerrito is not there.

But in California broadly, persistent structural imbalance combined with pension pressure has contributed to:

• severe service reductions

• emergency borrowing

• reserve depletion

• layoffs

• fiscal distress declarations

Usually, the problem is not pensions alone.

It is:

• pensions

• rising labor costs

• deferred maintenance

• weak revenue growth

• economic downturns

all happening simultaneously.

The Real Issue Is Structural Alignment

Pensions themselves are not inherently irresponsible.

Cities should honor commitments made to employees.

The real issue is whether:

• revenues

• staffing models

• infrastructure obligations

• service expectations

• long-term liabilities

remain aligned over time.

What this budget reveals is not a city in immediate fiscal crisis but appears to be heading that way.

But it does reveal a city operating with increasingly limited financial flexibility while carrying substantial structural obligations from prior decisions.

And once flexibility disappears, local governments often become reactive instead of strategic.

What I see in El Cerrito’s budget is a city trying to move toward more disciplined long-term planning while still carrying substantial long-term obligations that will continue placing pressure on services, infrastructure, reserves, and taxpayers for years to come.