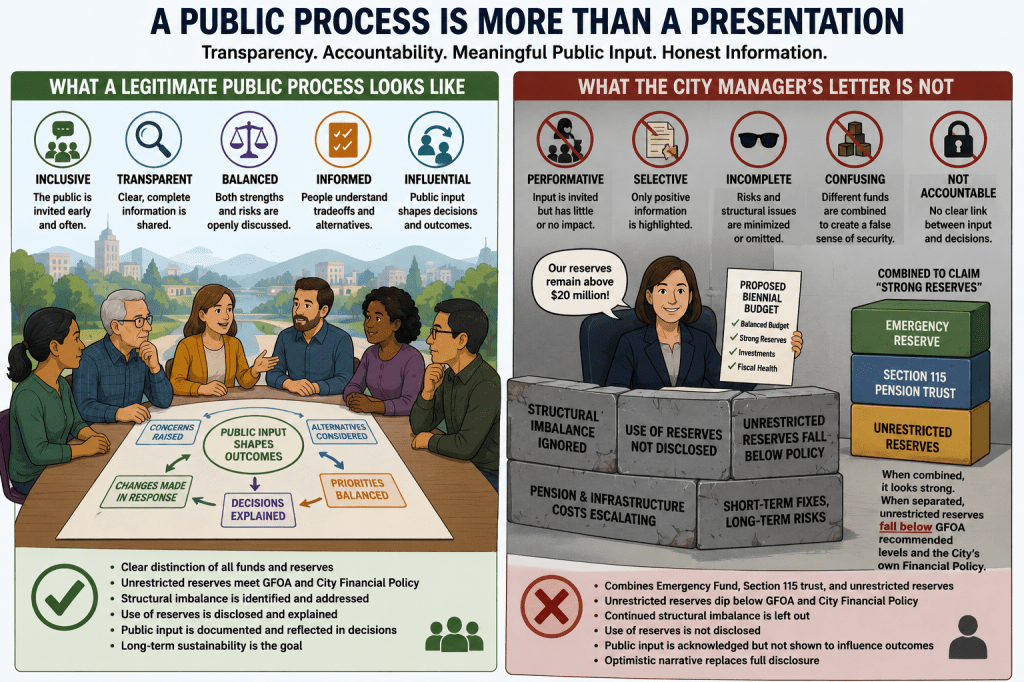

A legitimate public process is not simply a public meeting, a published agenda, or a polished budget presentation.

A legitimate public process is transparent, complete, balanced, and honest about both strengths and risks.

It gives residents enough information to understand not only what is being proposed, but also what is being deferred, understated, omitted, or shifted into the future.

Most importantly, a legitimate public process allows public input to meaningfully influence outcomes.

Public engagement is not legitimate if residents are invited to speak only after major assumptions, priorities, and financial directions have effectively already been decided behind closed doors.

It is not enough to hold workshops, accept comment cards, or allow public testimony if the outcome appears largely predetermined regardless of what the public says.

A real public process demonstrates how public feedback shaped the final recommendations.

Residents should be able to clearly identify:

- what concerns were raised

- what alternatives were considered

- what changes were made in response to public feedback

- what recommendations were rejected and why

- how competing priorities were balanced

Without that connection between public participation and actual decision-making, the process becomes performative rather than collaborative.

That is why the City Manager’s budget letter deserves careful scrutiny.

The letter repeatedly frames the proposed budget as evidence of “stronger financial footing” and “long-term fiscal health.” Residents are told the budget is balanced, reserves remain above $20 million, and the City is making investments in infrastructure, facilities, and public safety equipment.

But a legitimate public process requires more than highlighting positive talking points.

It also requires openly discussing the structural concerns that continue to appear throughout the budget itself.

The City’s financial challenges did not disappear simply because the budget technically balances on paper.

The underlying structural imbalance between recurring revenues and long-term expenditure growth remains a significant concern.

That distinction matters.

Balancing a budget for the next fiscal cycle is not the same thing as resolving the City’s long-term financial trajectory.

The budget itself acknowledges escalating pension obligations, inflationary pressures, rising operating costs, infrastructure liabilities, insurance increases, and continued dependence on expenditure controls and containment measures.

Several balancing strategies appear to rely heavily on reallocations, delayed obligations, operational containment, and optimistic future assumptions rather than permanent structural solutions.

Those are not minor details.

They are central to understanding the City’s actual fiscal condition.

Equally important, the discussion surrounding reserves lacks critical distinctions that residents deserve to understand.

The City Manager references maintaining reserves above $20 million over the next five years. However, that figure combines several very different categories of funds, including:

- the Emergency Disaster Relief Fund (EDRF)

- the Section 115 Pension Trust

- unrestricted operating reserves

- other designated or committed reserve categories

Those funds are not interchangeable.

The Emergency Disaster Relief Fund exists to respond to emergencies and disasters.

The Section 115 trust is a pension stabilization vehicle intended to help offset future pension volatility and unfunded retirement liabilities.

Neither fund functions the same way as unrestricted operating reserves available to address ordinary fiscal instability or unexpected operational deficits.

That distinction matters because combining these categories into a single large reserve number can create the impression that the City’s unrestricted financial flexibility is stronger than it actually is.

The City reportedly maintains approximately $8 million in the Emergency Disaster Relief Fund and approximately $3 million in the Section 115 Pension Trust alone.

When those designated and restricted balances are separated out, the City’s unrestricted reserves appear materially weaker relative to both Government Finance Officers Association reserve recommendations and the City’s own adopted financial policy targets.

Residents deserve to clearly understand that difference.

A legitimate public process would distinguish between:

- unrestricted operating reserves

- emergency reserves

- pension stabilization trusts

- committed or designated funds

- one-time resources versus recurring revenue

It would also clearly explain:

- whether reserves are projected to decline over time

- how sustainable current spending patterns are

- what happens if revenues soften during an economic downturn

- what future pension and infrastructure obligations may require

- whether current balancing strategies are temporary or permanent

Instead, the public is presented with a highly optimistic narrative that emphasizes stabilization while minimizing ongoing long-term risks.

That is not transparency.

Transparency means discussing both accomplishments and vulnerabilities.

Transparency means acknowledging that expenditure containment alone does not necessarily resolve a structural imbalance when long-term expenditure growth continues to outpace sustainable recurring revenues.

Transparency means openly discussing pension escalation, deferred liabilities, infrastructure needs, insurance inflation, labor pressures, and economic uncertainty.

Transparency also means helping residents understand the difference between short-term budget balancing and long-term fiscal sustainability.

None of this means the City should not invest in services, facilities, or public safety.

None of this means staff did not work hard on the budget.

And none of this means the decisions facing the City are easy.

But public trust depends on residents receiving the full picture — not simply the most politically favorable portions of it.

Residents should not have to piece together critical fiscal realities by reading between the lines of financial tables, reserve schedules, and footnotes.

Those realities should be openly explained.

Most importantly, residents should be able to see how their participation shaped the final budget itself.

If the community raised concerns about escalating costs, reserve usage, structural imbalance, deferred obligations, or long-term sustainability, the public should be able to identify where and how those concerns influenced the final recommendations.

Otherwise, public engagement risks becoming little more than a procedural exercise.

A real public process is not measured by how many meetings occur.

It is measured by whether residents are given enough honest, complete, and transparent information to make informed judgments about the City’s future — and whether their participation genuinely matters once they do.